From the Lab: A Simple Robust Gold Volatility Capture Model That Held Up Since 2002

A long-only 15-minute GC strategy with no entry filter, built to capture expansion in the day session, with 877 trades, 1.80 profit factor, and 1,570% return to max drawdown.

Research and education only. Results are hypothetical and based on backtests and simulations. Past performance does not predict future results. Futures and derivatives involve significant risk. Test on your own data, costs, execution, and infrastructure before trading.

💬 Message to readers

This week’s issue is a Gold day trading model, and what makes it interesting is what it doesn’t do.

There is no trend filter. No regime filter. No higher timeframe confirmation. No stacked conditions trying to look clever.

It is a pure volatility capture strategy.

That is what I like about it.

Most systems try to filter the market to death before they allow a trade. This one takes the opposite route. It accepts that Gold has a habit of doing one thing very well: sitting quiet, then expanding hard. Instead of trying to predict when that move should happen, the strategy simply positions itself to catch it when it does.

And Gold is a very good market for that kind of idea. It is active enough, emotional enough, and explosive enough that you do not always need a complex filter to extract something useful. Sometimes the move itself is the edge.

The structure is also clean. One long entry concept. One hard stop. One trailing stop. Flat by the close.

That is exactly the kind of system I like in a portfolio. Not because it is flashy, but because it is simple enough to trust and robust enough to matter.

The other interesting piece here is the session template. This strategy runs on a custom 09:00 to 15:30 session. That means it can suit traders using day-rate margin, and it can also fit prop firms that only allow day session trading. Of course that comes with its own risk. Day-rate margin can disappear when volatility spikes, so you still need to respect that. But from a practical trading point of view, this is a very usable structure.

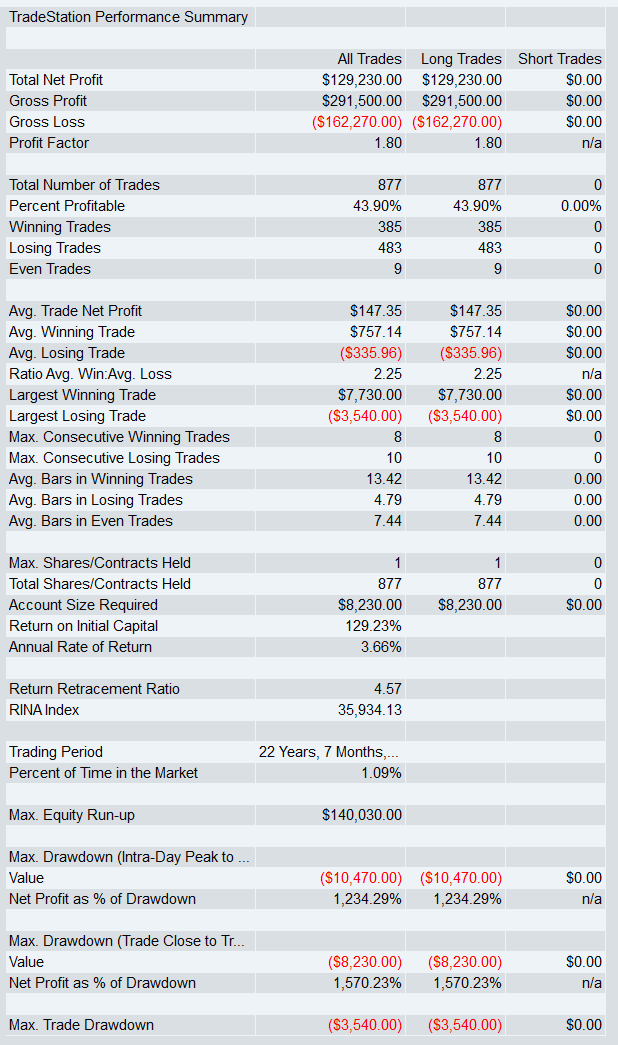

And the numbers are strong enough to take seriously. Since 2002, the strategy produced 877 trades, $129,230 net profit, a 1.80 profit factor, a 43.90% win rate, and 1,570.23% net profit to max closed-trade drawdown. That is a very respectable profile for a simple long-only intraday Gold system.

📖 The Idea

The idea is very simple.

Gold often spends time compressing, then suddenly expands. This strategy is designed to catch that expansion when it breaks out.

There is no entry filter deciding whether conditions are “good enough.” The strategy simply places a buy stop above price using recent volatility and lets Gold do the rest. If the market expands, it gets pulled into the trade. If not, nothing happens.

Once in the trade, risk is managed with a tighter ATR stop and then a much slower trailing ATR stop. Everything is closed by the end of the day.

That is the whole model. No prediction. No regime guessing. Just volatility expansion, risk control, and daily flattening. The code reflects exactly that structure: a long-only breakout entry above the current bar high plus an ATR-based offset, then a hard stop, a trailing stop and exits at 15:00.

🧠 Why this works for Gold

Gold is one of the better markets for a clean volatility breakout.

It can spend hours doing very little, then suddenly trend with real force. When that happens, the move is often clean enough that you do not need layers of filtering to capture it. You just need a sensible way to define the breakout and a sensible way to manage the risk afterward.

That is what this model is doing.

It is not trying to forecast direction in advance. It is waiting for Gold to expand and then joining the move once price proves it can break beyond its recent range.

🎯 Why I like it in a portfolio

I like this one because it does one job clearly.

It is not a mean reversion model. It is not a trend filter model. It is not a portfolio of conditions pretending to be a strategy. It is a straight volatility capture model for Gold.

That gives it a nice role inside a broader portfolio.

If you already run index systems, bond systems, or counter-trend ideas, this gives you something different. It is long only, session-based, and focused on expansion. That helps from a diversification point of view.

It is also practical. Because it runs on the 09:00 to 15:30 template, it is far more usable for traders who need to stay inside day-session rules. That opens the door for day-rate margin users and some prop-style environments. Again, that is not risk-free brokers can remove reduced margin in fast markets but from a workflow point of view it is a very tradable setup.

📈 Results of strategy since 2002

Since 2002, the strategy produced:

Net profit: $129,230.00

Profit factor: 1.80

Trades: 877

Win rate: 43.90%

Average trade: $147.35

Max closed-trade drawdown: $8,230.00

Return to max closed-trade drawdown: 1,570.23%

Trading period: 22 years, 7 months

Time in market: 1.09%

That is a strong profile for a simple, long-only Gold day model.

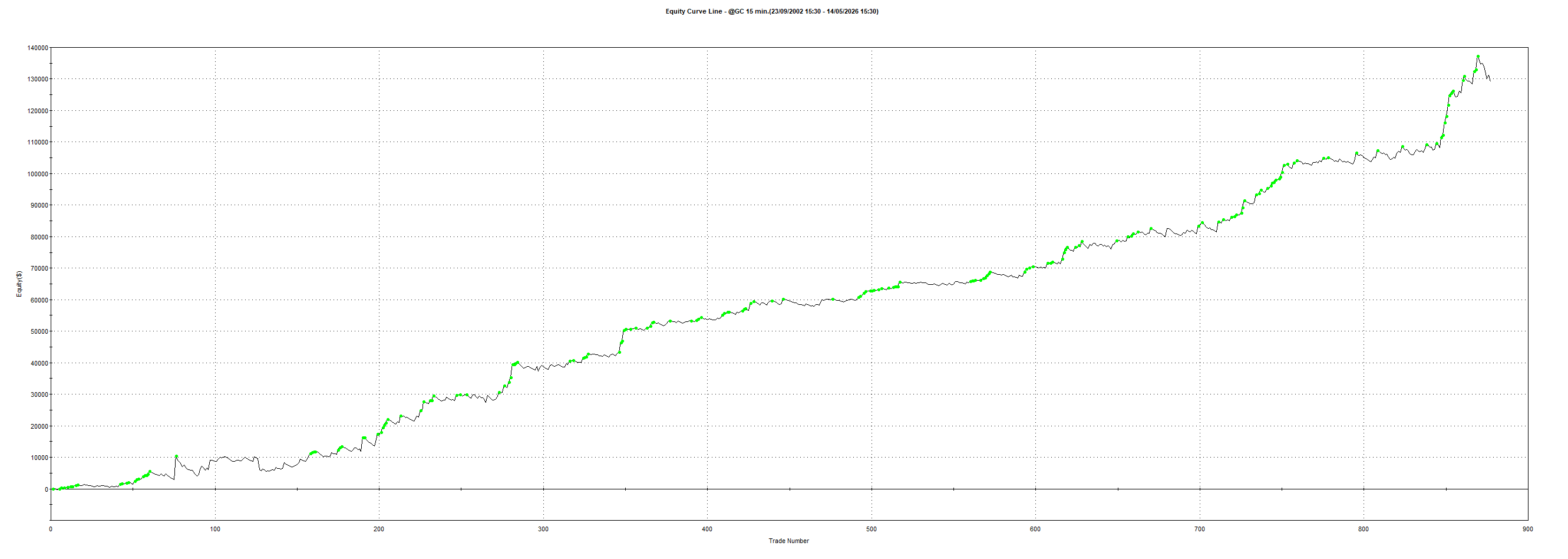

Results of strategy

Equity of strategy

The equity curve is what you want to see from this type of model. It is not relying on a handful of trades. It keeps stepping higher over a long sample.

🧪 Robustness testing

I trust a strategy only after it survives the usual stress tests.

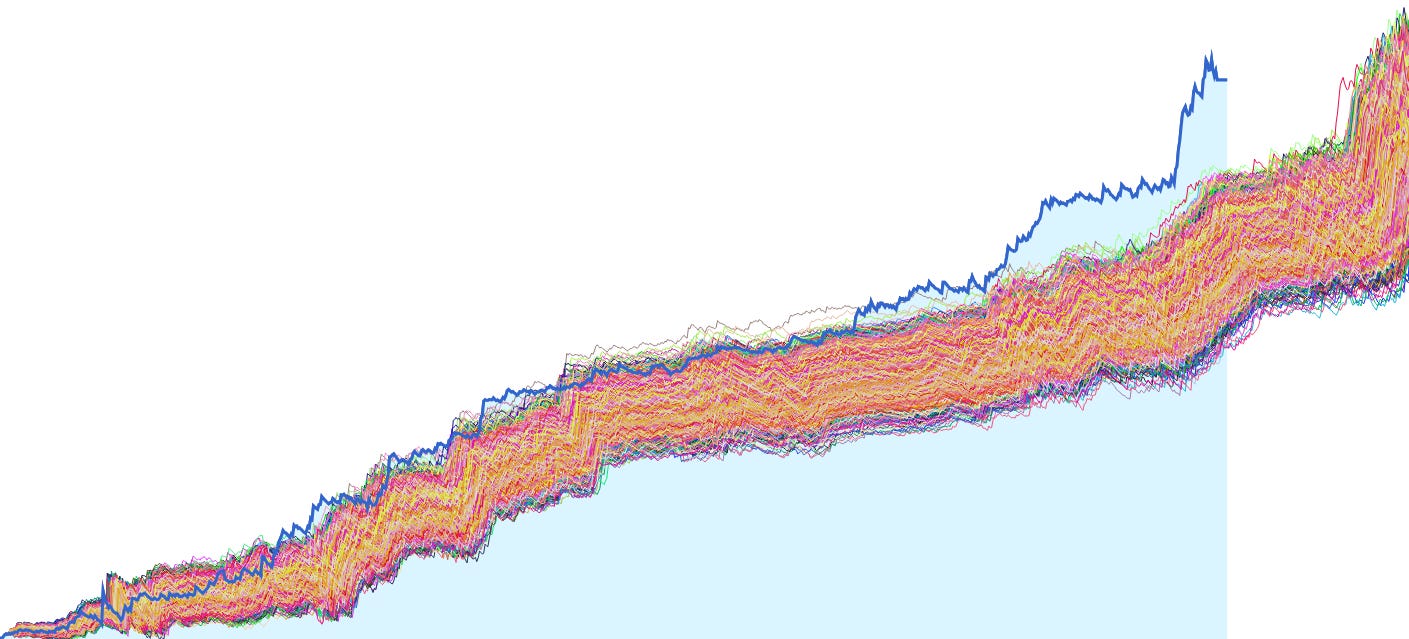

Monte Carlo OHLC

Here we adjust the structure of the bars and re-run the strategy across 10000 simulations.

This is one of the more useful tests for a breakout model. If the edge disappears as soon as you disturb the bar structure, it is fragile. If it keeps holding together, that is a much better sign.

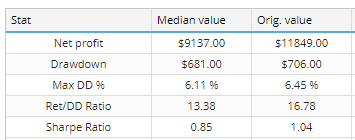

System Parameter Permutation test

We run many nearby combinations around the chosen settings.

This one is especially interesting here. The permutation work suggests the original result is somewhat overstated and that the median expectation is the more realistic number to focus on. That is exactly how it should be read. The good news is that the median result is still very solid, which is what matters most.

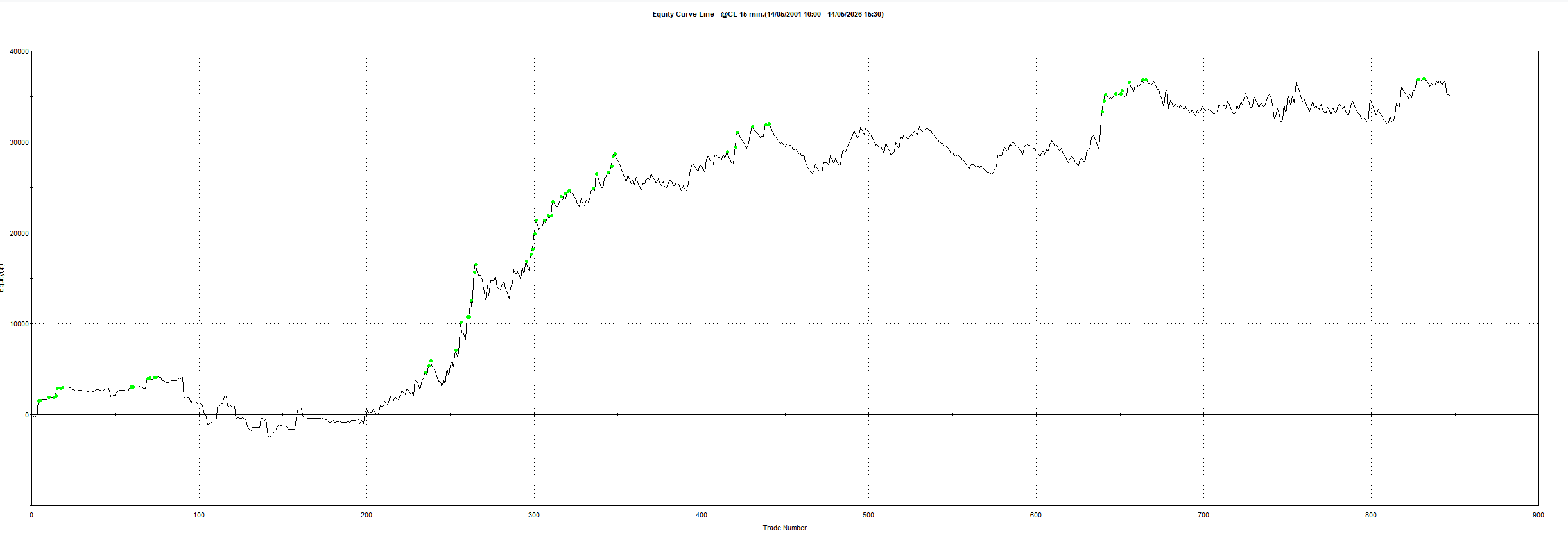

Alternative market test: CL

We apply the same logic to crude oil without redesigning it.

If the results are still acceptable, that tells us the idea is broader than just one market and less likely to be overfit to GC alone.

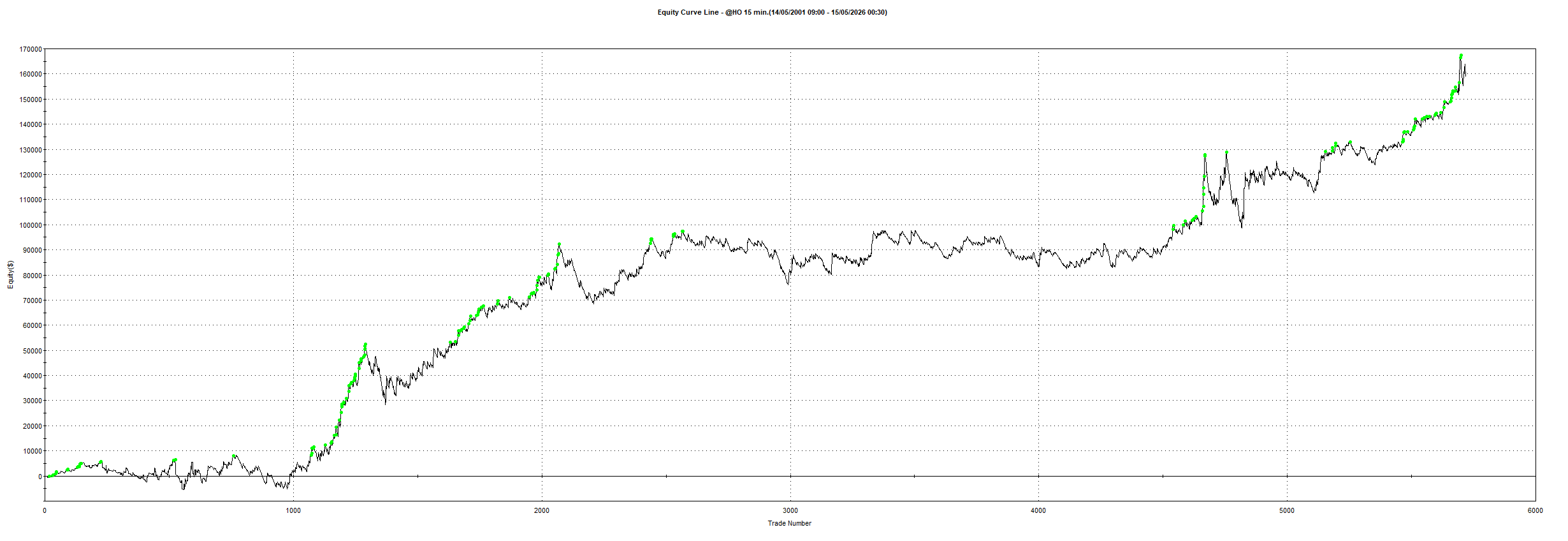

Alternative market test: HO

We apply the same logic to heating oil without redesigning it.

Again, we are not looking for perfection here. We are looking for evidence that the concept has legs outside one symbol.

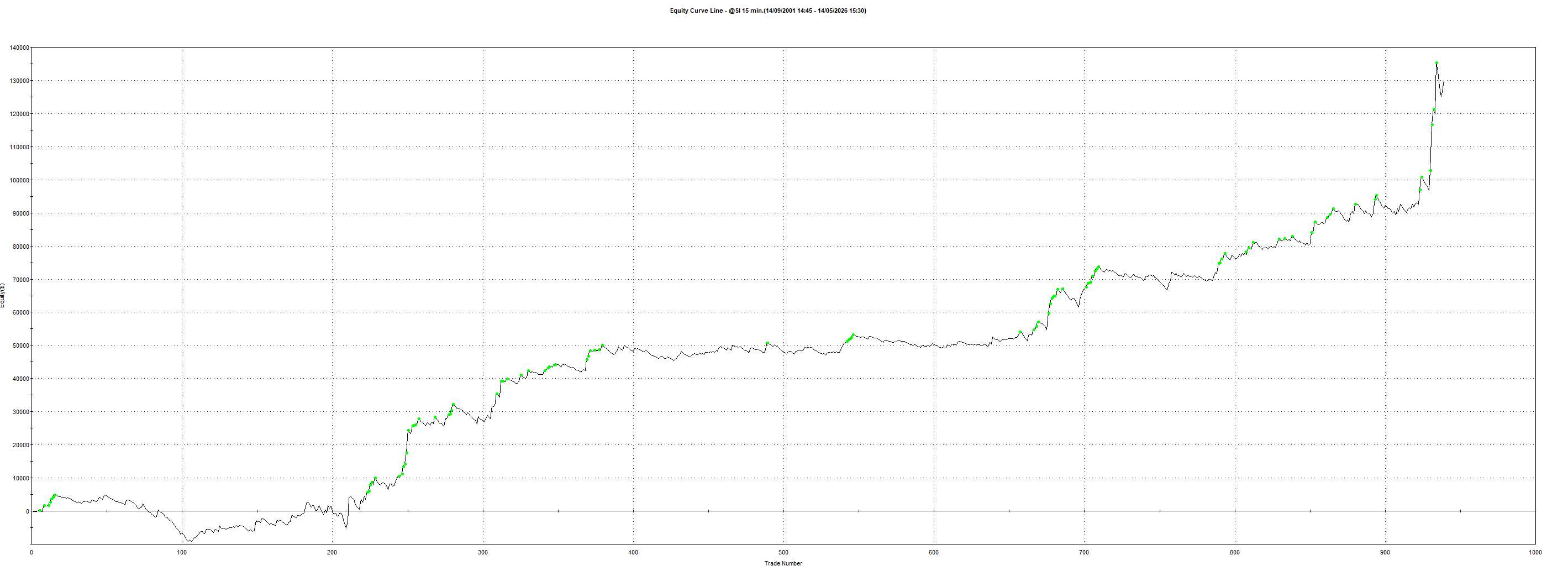

Alternative market test: SI

We apply the same logic to silver without redesigning it.

That is a particularly relevant test because silver is related to Gold but still behaves differently enough to tell us something useful.

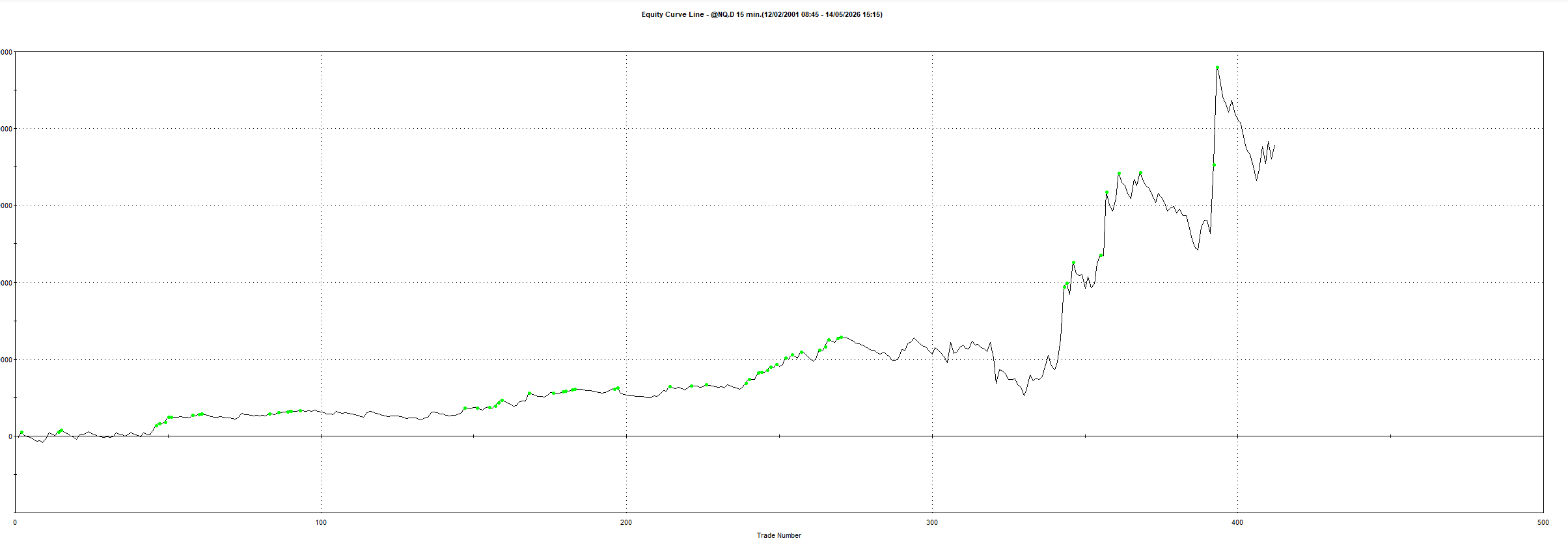

Alternative market test: NQ

We apply the same logic to NQ without redesigning it.

If it still produces something acceptable, that is another sign the core idea is broader than one market.

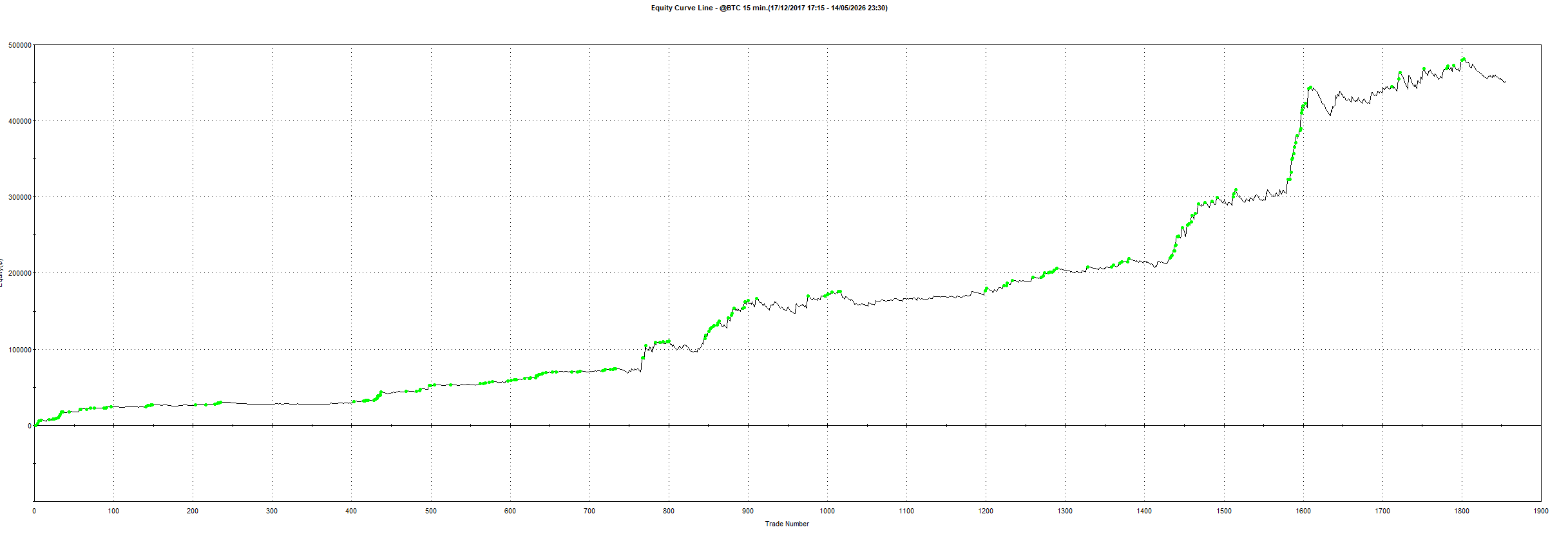

Alternative market test: BTC

We apply the same logic to BTC without redesigning it.

This is not because BTC and Gold are the same. It is because both can produce strong volatility expansions, and it is useful to see whether the breakout logic can travel.

Ready to put it to work? The full EasyLanguage code is below.

Dont forget this code can be easily converted to any other trading platform using LLMs and of course this can be run on Micro aswell.

By request, I’ll now include a clear plain English breakdown of each strategy with every parameter so you can rebuild it on your platform.